Buying your first home is an exciting step, but it can feel like a maze at times. Here's how it works, what you'll need to know and how to get ready. You're not just buying a home, you're starting a new chapter and we're here for you every step of the way.

Make the path to home ownership smoother

Whether you're ready to buy now, or just mulling things over, My First Home has plenty to help you.

- See how much you could afford to borrow.

- Figure out how long it could take you to save your deposit.

- Find out how to apply for a mortgage.

- See your credit score and learn ways to improve it.

- Get handy house hunting tips.

- Learn about the offer stage and what comes next.

You’ll find My First Home in our Mobile Banking app under ‘More options’. Or you can start your journey online.

Buying your home isn’t just one big leap. It’s a series of smart moves that add up.

A good place to start is with your credit score

Before you speak with a mortgage adviser or book any viewings, check your credit score.

It’s worth knowing where you stand early, as lenders will look at you more favourably if your credit score’s in a good place.

You can see your credit file In My First Home in our mobile app. Or check direct with Experian, Equifax and TransUnion to make sure everything looks just right.

If your score isn’t where you want it yet, that doesn’t mean buying a home’s off the table. It just means you’ve got a bit of work to do. The earlier you start, the more time those changes have to make a difference.

Ways to boost your credit score

- Make sure you’re registered to vote

- Cancel any unused credit cards or bank accounts.

- Keep your credit card and loan debts as low as you can. It’s important to show some responsible credit usage, so don’t avoid it completely.

- Avoid making late payments or missing them altogether.

None of this is glamorous, but it moves you forward.

Work out what you could realistically borrow

Your affordability is usually based on:

- how much you earn

- your day-to-day living costs – we'll work this out for you based on the national average

- any regular payments – for example, a monthly car payment

- whether you’re buying on your own or with someone else.

Once you’ve got a clearer picture, use our How much could I borrow calculator to see what’s realistic.

Now it’s time to get serious about your deposit

Knowing how much you could borrow turns a rough idea in your head into something to aim for when it comes to your deposit.

Let’s say you find out you could afford a home worth £300,000.

- A 10% deposit would be £30,000.

- A 5% deposit would be £15,000.

If your deposit's not all there yet, and everything in life is competing for your cash, rewarding your progress really matters. This is where our First Home Saver comes in. Take money out 2 times or less in 1 month, and you’ll get a better savings rate.

It’s also worth creating a savings plan. With My First Home, you can create a ‘property goal’ and work out how long it will take to squirrel away enough for a deposit. Try it on our website or in our app.

Different lenders offer different rates and types of mortgages, but all mortgages have a few things in common.

- You’re charged interest on the money you borrow.

- The higher the mortgage rate, the more interest you pay.

- The quicker you pay off your mortgage, the less interest you pay.

Most lenders offer terms up to 40 years. There’s no ‘right’ answer. It depends on what matters more to you – lower payments or being mortgage-free faster.

And your deposit? The bigger it is:

- the better deal you’re likely to get

- the less you need to borrow

- the lower your risk of negative equity (where your home is worth less than what you owe).

Fixed or tracker – what’s your pick?

At its core, the type of mortgage you go for depends on whether you want predictable payments or you’re comfortable with change.

Fixed rate mortgage

If you like knowing exactly what’s leaving your account each month, then a fixed rate gives you that clarity.

- Monthly payments stay the same during your initial rate period.

- Initial rate periods we typically offer – 2, 3, 5 or 10 years.

- After that, you’ll move to our Standard Variable Rate.

- You can usually overpay up to 10% of the fixed rate loan balance each calendar year (January to December).

- If you pay back more than that, or leave early, you’ll pay an early repayment charge (ERC).

For example, if the balance left on your fixed rate mortgage is £250,000, you could overpay by up to £25,000 that calendar year (10%) with no ERC.

You don’t have to do it in one go. You could make smaller overpayments across the year – for example, using a bonus or extra savings.

Of course, overpayments are optional and not expected. As a first time buyer, we know getting comfortable with your standard mortgage payment will be your main focus to begin with.

Tracker rate mortgage

This tracks above the Bank of England base rate, which is essentially the benchmark rate for borrowing money in the UK. They can work in your favour if rates fall. But your payments can go up if rates rise. You need to be comfortable with that movement.

- Initial rate period – typically 2 years.

- Moves to our Standard Variable Rate after that.

- Unlimited overpayments.

- No early repayment charge.

There are also lifetime tracker mortgages too, but you can't get one with us if you're taking out your first mortgage.

Other ways to make buying work

If buying on your own feels tight, or your deposit isn’t as big as you’d like, there are other options.

Buying with someone else

With us, you can buy with up to 3 other people (if you apply over the phone). This could increase how much you may be able to borrow, if your income alone is proving an issue. It can also make sharing the cost of a mortgage more manageable. But this is a long-term commitment. You need to trust that:

- they’ll keep up their end of the bargain – in other words, make their part of the payment

- you’re both clear on what happens if one of you wants out.

If you’re thinking about taking this route, make sure you get proper legal advice before going ahead.

There are 2 ways to own a property with your partner, family member or friend.

Joint tenants

As joint tenants (sometimes called ‘beneficial joint tenants’):

- you have equal rights to the whole property

- if one of you dies, their share automatically passes to the other

- you can’t leave your share to someone else in a will.

Tenants in common

As tenants in common:

- you can own different shares of the property

- your share doesn’t automatically go to the other if you die

- you can leave your share to whoever you want in your will.

Gifted deposits

A family member or friend can gift you money towards your deposit. They can use savings, or even raise money against their own property. You can put some or all of their gift towards your deposit.

This could help speed things up so you’re ready to buy sooner. Just make sure everyone’s clear it’s a gift, as you’ll be asked for proof of this later down the line.

Shared Ownership

This lowers the upfront hurdle. You buy part of a home, and a housing association owns the rest. You pay rent on the share you don’t own.

Over time, you can buy more shares (known as staircasing), until you own 100%. But you’ll be balancing paying a mortgage with rent on top.

Our Shared Ownership page tells you more.

Government schemes

We take part in some schemes to help people onto the ladder.

Forces Help to Buy

For regular Armed Forces personnel.

- Run by the Ministry of Defence.

- Can’t be combined with other mortgage schemes.

- Works like a standard mortgage.

- You’ll need to call us to apply.

Find out more about Forces Help to Buy.

Help to Buy ISA

If you already have one:

- you can keep saving into it until 30 November 2029

- your conveyancer must claim your 25% government bonus by 1 December 2030 (eligibility applies – check the Help to Buy government website).

This scheme is closed to new applicants.

Ways to repay your mortgage

Mortgage payments are made up of:

- The capital – the amount you originally borrowed to buy your home.

- The interest – what the lender charges you for borrowing that money.

When you take out a mortgage, you’ve got the choice of 3 ways to pay it back.

Repayment mortgage (sometimes called ‘capital and interest’)

Your mortgage payment covers the interest and reduces the amount you owe (as capital). As long as you keep up your payments, your mortgage will be fully paid off at the end of the term.

Interest only mortgage

Your monthly payment covers just the interest. The amount you borrowed isn’t paid off, so you’ll need a plan to pay back the full balance at the end of the term. For example, selling your home and downsizing or using investments.

If you choose interest only, you’ll need to be confident you’ll have enough set aside to clear the balance when your mortgage ends.

Part repayment, part interest only

Your mortgage is split into separate loans. One part goes down over time (repayment), and the other part doesn’t (interest only).

Let’s say you borrow £300,000 to buy your home.

- £200,000 is on a repayment basis.

- £100,000 is on an interest only basis.

Each month:

- you pay off capital and interest on the £200,000, so that part gradually goes down

- you pay interest only on the £100,000, so that amount stays the same.

By the end of your mortgage term:

- the £200,000 repayment portion is fully paid off (as long as you’ve kept up your payments)

- the £100,000 interest only portion still needs to be paid back in full.

That means you’d need a plan to pay back £100,000. For example, through investments or selling your home.

What fees will you need to pay?

Your monthly payment isn’t the only cost. There are a few others to factor in – some paid upfront and some added to the mortgage.

We’ve listed the main ones here, but you should check with your mortgage lender, solicitor or surveyor to see if there are any others.

Product fee

Think of this as the cost of securing your particular mortgage rate. Some mortgages don’t have one. Others do, often because the rate is lower.

So you’re effectively choosing between:

- higher rate, no fee

- lower rate, but you pay a fee.

The fee is typically a fixed amount (for example, £999), not a percentage of the mortgage.

You can pay it upfront when you apply or add it to your mortgage. If you add it to your mortgage, you’ll pay interest, unless you pay it back within 21 days of the mortgage starting.

We offer a range of mortgages with and without a product fee.

Valuation

This checks it's suitable for a mortgage based on what you're paying for it. Most of our mortgages offer a free standard valuation.

Survey

A survey gives you a more detailed view of the property’s condition. Costs vary depending on the type of survey you choose. UK surveyors are governed by The Royal Institution of Chartered Surveyors (RICS).

Legal and conveyancing fees

Conveyancing is the legal work involved in transferring ownership of the property. You’ll need a solicitor or a licensed conveyancer for this.

They’ll also carry out property searches. For example, checking for planned developments nearby.

Always get a quote upfront, and make sure you check what’s included.

Stamp duty

If you’re buying a home in England or Northern Ireland, you might need to pay Stamp Duty Land Tax (SDLT) to HM Revenue and Customs (HMRC). The amount will depend on the price of the home you’re buying. If you’re a first time buyer, you’ll only pay Stamp Duty if you’re buying a home worth more than £300,000.

View current rates on the government’s Stamp Duty Land Tax page.

Different taxes apply in Scotland (Land and Buildings Transaction Tax) and Wales (Land Transaction Tax).

Removal costs

Moving costs can vary. Get a few quotes and check what’s included – packing, insurance and vehicle size.

Account fee

You might pay an account fee to your chosen mortgage lender. It’s a fixed fee and covers the cost of setting up your mortgage and managing it behind the scenes.

You usually pay it when your mortgage starts, or you can choose to pay it at the end of the mortgage term instead. The fee itself won’t change if you delay the payment to the end of your mortgage.

How much could I borrow?

How much deposit will I need to save?

Where does my money go each month?

First Home Saver

Saving for your first place? Protecting your progress matters.

Our First Home Saver makes it less tempting to take from your savings. Take money out of your savings 2 times or less in 1 calendar month and you'll get a better rate.

Plus your chance to win £10,000. Each month from May to December 2026, we’re giving £10,000 to 1 lucky person who has a First Home Saver with us. Every £100 increase in your balance that month equals 1 entry. Aged 18+. T&Cs apply.

Once your credit’s solid, your deposit’s almost there and you’ve sense checked how much you could borrow – it’s time to get your decision in principle (DIP).

It lets you know if you can borrow what you want before you do a full mortgage application. It’s also known as:

- a mortgage in principle

- an agreement in principle

- a mortgage agreement in principle.

Having a DIP also shows estate agents you mean business, so you can start booking viewings.

You can get a DIP from us today. It's free and valid for 60 days. It doesn't mean you're tied to going with us as your mortgage lender, but it gives you something to get the ball rolling.

If you do decide to go with us later down the line, having a DIP gives you a head start on a full mortgage application.

Looking for a home

When you start looking, it helps to have a clear idea of what matters to you.

Think about the basics first.

- What type of property – flat, terrace or new build?

- How many bedrooms and bathrooms?

- Do you need outside space?

- Is parking a deal breaker?

It’s tricky to find a home that ticks every single box. So it’s worth knowing what’s non-negotiable and what’s just a ‘nice to have’.

Then zoom out from the house itself – what about the area?

- How close is it to work or public transport?

- Are there shops, gyms and cafés nearby?

- If schools matter now or in the future, what are they like?

Try to visit at different times of day if you can. A quiet weekend viewing won’t tell you what it’s like at rush hour on a weekday.

And ask questions at viewings. Lots of them. After all, there’s a chance this could be your home.

House hunting tips

- Take someone with you. A second pair of eyes always helps.

- It’s surprisingly easy to get distracted by a fancy kitchen and forget the practical stuff – so note down a few questions to ask. Download a copy of our home viewer’s checklist (PDF - 32 KB) that gives you something to work with.

- Remember – the estate agent works for the seller, not you. They must be honest and accurate, but they’re paid to sell the property. It’s easy to see everything through rose-tinted glasses when you love a place, but make sure it stacks up on the practical stuff too.

- Check the Energy Performance Certificate (EPC). It shows how energy efficient the property is. In theory, the better the rating on an EPC, the cheaper your house will be to run. For new builds, you should be given a Predicted Energy Assessment.

- If the property is a leasehold, you’ll need details like how many years are left on the lease, plus any ground rent or service charges.

Making an offer

Once you’ve found somewhere you love, it shifts from browsing to getting down to business.

Hopefully you’ll already have a number in your head. Not just what you want to pay, but what you can realistically offer based on your deposit and your decision in principle.

Here are a few things to keep front of mind ahead of making an offer

- Check what similar places in the area have sold for. Asking price is one thing, sale price is another. This also avoids you paying over the odds for your home, or lowballing the seller with your offer.

- Decide the absolute maximum you’re willing to offer, in case there’s a bit of back and forth. If the property is a real catch, it’s likely you’ll be up against other potential buyers. Emotions can rise fast once you’re in it, so try not to get caught in a bidding war. Equally, the seller may counter. If this happens, you’ve got a choice – hold firm, increase your offer, or walk away.

- If you’re a first time buyer, make it clear that you’re chain free, with a decision in principle sorted and your deposit good to go. Speed and certainty can be as powerful as a slightly higher offer.

When you’re ready, you’ll make your offer through the estate agent. It’s usually verbal to start with, but they may also ask you to put it in writing – so it helps to have a draft email ready to go. They’ll then take it to the seller and come back to you.

Sometimes it’s accepted straight away. More often, there’s a bit of back and forth. Or sadly, it might be rejected.

If it’s accepted, you’ll need to choose a solicitor. They’ll handle the legal side of things, like contracts, searches and transferring ownership. Essentially, they’ll make sure everything is done properly, the sale goes through and you become the legal owner.

In England and Wales, an accepted offer isn’t legally binding – in other words, it can still fall through.

In Scotland, things are a bit different. Once your offer’s accepted, you’re committed.

- Properties are advertised at a fixed price or an 'offer price'. This price isn’t always what it will sell for, so be clear on what you can afford and what you believe it’s worth.

- Read the Home Report carefully and make sure your mortgage is lined up before you put an offer in.

- If the seller accepts your offer, it becomes legally binding. They can’t accept a higher price from someone else after that.

- The formal offer and acceptance are set out in formal letters known as 'missives’.

Once your offer’s accepted, this is where it gets real.

You’ll need to take your decision in principle one step further and get a full mortgage application sorted.

If you choose to go with one of our mortgages, you can apply online or over the phone. Either way, having everything ready upfront makes this a smoother process.

What you’ll need

- Your last 3 years’ address history, with no gaps.

- If you’re employed, your last 3 months’ payslips.

- If you’re self-employed, your last 3 years’ accounts or SA302s and Tax Year Overviews.

- Your last 3 months’ personal bank statements.

- Full details of any loans or credit cards you have.

- ID, such as your driving licence or passport.

It’s admin heavy. But you’ll thank yourself later for getting organised. And of course, we’re here to make it as hassle free as we can.

Applying online

You can apply online if:

- you’ve already got a decision in principle from us

- your offer’s been accepted.

You don’t have to apply in one go. You can save and come back to it if you need to.

You’ll see the deals you may be able to get, including monthly payments and any fees.

Once you’ve chosen a deal, you’ll get a mortgage illustration. This is your quote that shows the costs of the mortgage and any fees.

When you’re finished, you’ll get an instant decision – subject to document checks and a satisfactory property valuation.

This is the quickest way to apply. But you’ll need to feel confident deciding what you want from your mortgage without our advice.

Applying over the phone

If you'd rather talk it through, you can speak to our mortgage team once you've had an offer accepted. You'll get free advice about our mortgages over the phone or by video call wherever you feel most comfortable, whether that's at home or on the go.

They’ll:

- ask about your needs and circumstances

- check the mortgage is affordable

- recommend a suitable option from our range

- take some details about the property and your solicitor.

Call us on 0800 068 6064. We're here Monday to Friday 9am-6pm and Saturday 9am-2pm

You’ll then get a mortgage illustration for the recommended mortgage deal, setting out the costs and fees.

Property valuation

After you apply, we’ll value the property for you. This confirms it's suitable for a mortgage based on what you're paying for it.

The way we value your property will depend on the type of mortgage you need and the amount you’re borrowing.

It could be:

- an automated valuation, or

- a visit from an independent registered valuer, who will inspect the property externally or internally.

You'll get a copy of the report whichever way we value your new home.

A few important bits to note

- A mortgage valuation isn’t a survey. It doesn’t give you detailed advice on the property’s condition.

- If the valuer spots any issues, like cracking, damp or anything structural, we might need some further reports before we decide to give you the mortgage.

- The property must be habitable before we release the money. For a home to be habitable, it needs a working kitchen and bathroom as a minimum.

Once the valuation and any additional reports are satisfactory, we’ll make you a formal mortgage offer. That’s when it’s officially approved.

If you’re buying in Scotland, we might accept a transcription of the valuation from the seller’s Home Report.

Types of surveys

Separate from the lender’s valuation, we strongly advise you pay for your own survey.

It might not flag anything major. In which case, great – it’s given you peace of mind. Or it might uncover some issues. This doesn’t automatically mean walking away. It might mean renegotiating, budgeting for repairs, or deciding it’s not the one after all.

Either way, better to know before you’re in, keys in hand, discovering surprises you can’t afford.

You can find a surveyor through RICS and they’ll help you figure out which level is best.

Here’s a breakdown of the 2 main types.

Home Survey Level 2 Report

For standard properties in a reasonable condition.

- Covers the property’s condition.

- Highlights defects that could affect the value.

- Gives advice on repairs and maintenance.

- Flags legal issues to address.

- Gives details on the location and local environment.

Home Survey Level 3 Report

The most comprehensive report and provides in-depth analysis of the condition of a property.

For properties:

- that are larger, older or run down

- that are unusual or have been altered

- where there’s an intention to carry out major works.

Whichever survey you choose, it's for you, not us, and you can talk it through with your surveyor.

This is the bit no one posts about on Instagram. No glossy keys shot (yet!), just emails, documents and lots of waiting. But it’s the stage that actually gets you over the line.

Choosing a solicitor or conveyancer

Once your offer’s accepted, you’ll need a solicitor or conveyancer to handle the legal side of things.

If you decide to use us for your mortgage, we’ve got a list of approved solicitors and conveyancers in your area. Just give us a call and we can share this with you.

If you choose one that isn’t on our approved list, another firm will need to act on our behalf and you’ll need to cover that extra cost.

When choosing who to go with:

- ask for a full breakdown of costs, no vague estimates

- check they'll be available when you need them, as chains can move quickly

- ask how often they’ll update you and how – email, letters or phone.

You want someone responsive. Life’s busy enough without chasing legal updates late at night.

What the legal work involves

There’s more going on behind the scenes than you may realise. Progress might feel slow at times, but it’s there for a reason and protects what’s likely to be the biggest purchase you’ve ever made.

- Local authority search – for homes in England, Wales and Northern Ireland, this checks for anything that might affect your property, like plans to develop nearby land and roads. In Scotland, these checks are covered by the Property Enquiry Certificate (PEC) that the seller will provide with the Home Buyer Report.

- Drawing up and exchanging contracts – once you exchange (called Conclusion of Missives in Scotland), your deposit is transferred and you’re legally committed.

- Completion dates – agreed between you and the seller through your solicitor or conveyancer. This is when the purchase money is paid to the seller and the property officially becomes yours.

- Transfer and title deeds – after completion, your solicitor or conveyancer registers you as the legal owner. For England and Wales, they’ll also apply to update the title deed to prove you own the property. In Scotland, the title deeds are called title sheets (registered land) or sasine deeds (unregistered land) and registered with the Register of Scotland.

Exchange and completion

Your mortgage offer

Once your valuation is sorted and everything stacks up, you’ll receive your formal mortgage offer. It will look similar to your original illustration, but may include specific conditions you need to meet.

The contracts

When everything’s ready, you’ll be sent a contract to sign. Go through everything with a fine-tooth comb and make sure you’re happy. The seller will be doing the same their side.

Once both sides agree a completion date and exchange contracts (called Conclusion of Missives in Scotland), you’re legally committed.

If you’re renting, check your notice period before you agree a completion date. The last thing you want is to be paying rent and a mortgage at the same time because you didn’t time it right.

Check you have home insurance

In England, Wales and Northern Ireland, you’ll need buildings insurance in place for your new pad from exchange (for Scottish properties, it’s from completion). It’s a requirement to have buildings insurance in place for the life of your mortgage and it must be enough to cover the cost to rebuild your home should the worst happen. Your mortgage lender might ask to see a copy of your policy. It covers things like fire damage and flooding. You can sort your buildings insurance with us.

It’s also worth sorting contents insurance for when you move in. You’ve worked hard for what’s inside your new home, so protecting it makes sense.

If you’re renting, you might already have contents insurance. In that case, it could just be a case of updating your address rather than starting from scratch.

Completion

On completion day, the money will go across to the seller’s conveyancers. This normally happens on a weekday.

And then, the place you fell in love with, saved for, stressed over, is officially yours.

Buying your first home in the UK is a proper milestone – especially in a market that doesn’t exactly make it easy. It’s years of saving. Saying no to stuff. Watching your friends travel while you build a deposit. You should be super proud.

Time to collect the keys and move in!

Best Online Mortgage Lender 2025 - 2026

Helping customers brings out the best in us. That’s why we’ve won the Your Mortgage Best Online Mortgage Lender 2025-2026.

So, if you're buying your first home, you’re onto a winner with us.

Compare our mortgage rates

It’s quick and easy to compare our mortgage rates and see what your monthly payments could be.

Get your decision in principle online

See if we could lend you the amount you need. It’s free, no obligation and valid for 60 days.

Apply for your mortgage online

Got your decision in principle? You’re good to go ahead with a full application.

Need some help? Get free advice about Santander mortgages over the phone or by video call wherever you feel most comfortable, whether that's at home or on the go. We'll explain your options, answer your questions and help you feel confident about your next step. No pressure, just friendly support when you need it.

0800 068 6064 - 9am to 6pm Monday to Friday and 9am to 2pm Saturday

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE

Applications are subject to status and lending criteria. Applicants must be UK residents aged 18 or over. The amount we will lend depends on your circumstances, the amount borrowed and the property. A higher deposit may be required for a flat or new build.

Looking for a low deposit mortgage?

My First Mortgage could get you on the ladder with a £10,000 deposit.

First time buyer mortgages

Explore our first time buyer mortgage options to find one that best suits you.

When buying your first home, it’s important to make sure you put the right protection in place – should the worst happen.

Protect your new home

We've got you sorted with simple cover to protect your home and what's in it.

Administered and underwritten by Aviva Insurance Limited.

Protect your lifestyle and mortgage

Get a personalised quote in just 2 minutes.

If you have a Santander mortgage, and take out life insurance with us, we'll give you £150 cashback. Offer can be withdrawn at any time. T&Cs apply.

Administered and underwritten by Aviva Insurance Limited.

Before move in day, make sure you’ve contacted the gas, water, electricity and broadband providers for your new home, so everything’s working when you get there.

Take meter readings as soon as you move in. It takes 5 minutes and means you’re only paying for what you actually use – not the previous owner’s last long shower.

Your new address

You'll need to update your address with everyone from your GP to your bank and employer. Do this as soon as you can.

And here are a few other reminders. Even if you think you've updated everyone, something always slips through.

- The electoral register

- DVLA (Driver & Vehicle Licensing Agency)

- HMRC

- Council tax. You should aim to let your old and new council know within the first few weeks of being in your new home.

- Redirect your post from your old address

Your first mortgage payment might be higher than the one you saw in your offer. Don't worry, that's normal. Here's how it works using an example.

- You complete on 19 March.

- Your chosen payment date is the 1st of each month.

- The first payment will be taken on 1 April.

- This payment will include your normal monthly payment for April, and interest from 19-31 March (the extra bit).

This only happens on your first payment. After that, your payments will go back to what you expect, as long as your mortgage is on a fixed rate.

If you choose us for your mortgage, we'll send you a letter that explains this once your mortgage starts. You can also keep an eye on everything in our app. Managing your mortgage online whenever and wherever you like. It’s secure and easy to set up.

Once you’ve picked up the keys, you’ll want to get comfy in your new pad right away. So, we’ll connect you with partners who can help you move home and save money on your energy, broadband and TV. You’ll be settled in and ready to plan your housewarming party in no time.

Get your home connected

Explore top deals for your TV, broadband or phone.

See if you can save online or in My Home Manager.

Make moving day cheaper

First time buyers save 30% with AnyVan

Get a free quote and lock in your discount today.

T&Cs apply. Offer available 20 April-30 June 2026.

Some of the partners we work with will pay us commission. We aren't responsible for the products and services offered by our partners.

Check how efficient your home is in minutes and get some quick wins to use less energy.

Our Tomorrow’s Homes Hub brings practical fixes and trusted installers together in one place.

My Home Manager

- Spot ways to save on your bills.

- Track your home’s value over time.

- Tools to keep your home in good shape.

You’ll find My Home Manager in our app under ‘More options’

How do I switch to Santander?

We have a range of accounts designed to meet your needs.

Choose to switch to us when you apply, or anytime after opening a Santander account. We’ll do the hard work, like closing your old account and moving payments. It’s simple, reliable and stress-free.

Santander credit cards

Whether you’re managing everyday spending, transferring existing balances, or making your money work harder with cashback and rewards.

Discover a range of credit cards designed to help you pay smarter.

Remember, credit cards are a type of borrowing. If you don’t pay in full by the date on your monthly bill, you’ll be charged interest.

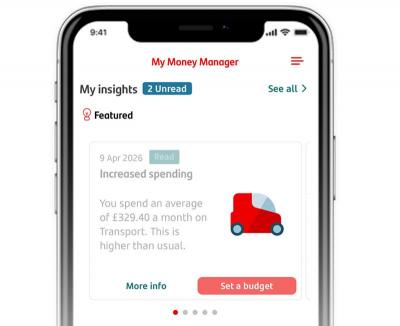

Keep your money in check

My Money Manager takes the guesswork out of things.

- Spot patterns in where your money’s going.

- Help with getting into good habits.

- Keep tabs on your subscriptions and budgets.

All super handy while buying your first home and beyond.

You’ll find My Money Manager in our Mobile Banking app.

We understand that one of the hardest things for first time buyers is getting enough money for the deposit. That’s why we’re saying it might not be as hard as you think. You might be able to buy your first home with a deposit from £10,000, but this will depend on your situation, as well as the property price, property type, location and the mortgage product available to you.

My First Mortgage

Our new My First Mortgage is available to first time buyers with a deposit of between 2% and less than 5% of the house value.

Product features

- Minimum £10,000 deposit.

- Maximum 98% loan to value

- Not available on flats, new builds or properties in Northern Ireland.

- Maximum loan £500,000.

What this means for a £10,000 deposit

So, if you put down a £10,000 deposit, it would be enough to buy a house between £200,001 and £500,000.

- £10,000 deposit on a £500,000 property is 2% of the property value.

- £10,000 deposit on a £200,001 property is 4.9% of the property value.

Our 5% deposit mortgages

For first time buyers with a deposit of between 5% and less than 10% of the property value. Available on houses, flats and new builds.

What this means for a £10,000 deposit

A £10,000 deposit would also be enough to buy a home between £100,010 and £200,000.

- £10,000 deposit on a £200,000 property is 5% of the property value.

- £10,000 deposit on a £100,010 property is 9.9% of the property value.

This means a £10,000 deposit could be used across a range of property prices.

When your deposit could even be less than £10,000

In the lowest property price locations, you might not even need a £10,000 deposit. For example, a 5% deposit on a £100,000 property is £5,000.

Important stuff to know

- £10,000 is a useful guide, but the deposit you need will depend on the property price, location and product eligibility. Plus it depends on your individual circumstances, such as whether you can afford the mortgage. Your biggest financial commitment shouldn’t be a burden.

- A higher deposit (for example 10%) reduces your loan to value even further and means you could pay a lower interest rate.

- Our mortgage advisers give you advice on the most suitable mortgage for you, which may include paying a bigger deposit amount.