The question of where you should put your money is an important one. There’s a lot of choice out there so it helps to approach this decision with a bit of structure.

All investments come with some degree of risk, that’s just a fact. So, if the plans you have for your money mean you can’t afford to or are unwilling to take any risks with it, investing is unlikely to be for you. Investment values go down as well as up and you can get back less than you put in. But the level of risk can vary considerably depending on the type of investments you go for.

As a general rule the more risk you take, the more you might get back. But the flip side is that you also stand a greater chance of losing at least some of your money.

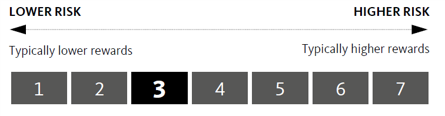

One way to think of it is as a sliding scale. Having some idea of where you’d feel comfortable on a sliding scale helps you narrow down your choices. There’s a standard scale you can use to compare options if you’re investing through a fund (we’ll come back to what a fund is later). It looks like this.

Often, companies that offer funds also have their own way of describing different risk levels for the funds they offer. Effectively their own sliding scale.

How long you’re intending to invest for, and how much money you can afford to lose, are worth thinking about when choosing where you want to be on the risk scale.

If you’ve got many years of investing ahead, you might be less concerned about short-term ups and downs in the value of your investment. That may mean you’re comfortable being higher up the risk scale which could increase your potential for getting more back.

Being lower down the risk scale could reduce that potential, but there’s also less chance of losing money. That would be an important consideration if you’re planning to access your money sooner rather than later, or if losing some or all of it would affect your standard of living.

It’s also key to diversify your investments to balance out some of the risks. Diversification is best described as not putting all your eggs in one basket. If you invest in a number of different assets or sectors, for example, you’ll be diversified so that it’s less likely that all of your investments will go up or down at the same time. You can also spread your risk within an asset class by investing in different geographic regions or business areas.

When your investments are well diversified like this your investment portfolio as a whole becomes less volatile.

Individual Savings Account (ISA)

Stocks and shares ISAs offer a tax efficient way of investing where your investments grow without being subject to Income or Capital Gains Tax.

For the 2026/27 tax year, you can save up to the annual ISA allowance (£20,000) in cash ISAs, stocks and shares ISAs, innovative finance ISAs and a lifetime ISA. Your ISA limit can be paid into multiple ISAs of the same type, except the lifetime ISA, each tax year.

You can transfer some or all the money you’ve built up in previous tax years and all the money you’ve paid into an ISA in the current tax year. From 6 April 2024, some providers may allow you to transfer some of your current tax year subscriptions, but Santander ISA Managers Limited does not offer this.

Investment account

An investment account is a simple way of holding investments. It has none of the tax benefits of an ISA but any capital gains you make can be offset against your annual Capital Gains Tax allowance.

Bond

A type of loan to a government or company over a fixed period which usually pays out a fixed amount of interest. Most bonds can be bought and sold during the loan period. And if you hold them when the loan is due to be repaid, you’ll get back the bonds’ original face value (which could be more or less than you paid for them).

The risks

Government bonds (known as gilts in the UK) can be lower risk than company (or corporate) bonds if you invest in a country with a good history of paying out on its bonds such as the UK, Switzerland or Denmark. The idea behind government bonds is that governments can be relied on to repay their debt. But they can also pay a lower interest rate as a result. If you invest in bonds from countries with a lower likelihood of repayment, you’re rewarded with a higher rate of interest.

Shares

Here you’re buying a stake in the fortunes of the company that issues them. Like bonds, shares can usually be bought and sold, but there is no underlying loan to be repaid. Shares can pay you an income (a dividend) but this isn’t usually guaranteed and can vary from year to year.

The risks

Shares can go up and down in value for various reasons, including people’s view of the company’s fortunes and how things like the economy might affect it. Ups and downs can be quite sharp, particularly over the shorter term.

Property

Investing in ‘bricks and mortar’ (or perhaps ‘stainless steel and glass’ these days) is another relatively popular option for investors. This can include a stake in commercial properties like hotels, offices or shopping centres. It’s common now to invest in property through property funds, which lowers risk by spreading it across a number of properties.

The risks

Property can generate high returns in the right market conditions but can be slower to sell than bonds or shares.

Whichever asset class you choose to invest in, the level of risk and potential return will vary by the geographic region and business area as each can be affected differently by unforeseen factors.

Geographic regions

It is understandable that different geographic regions will present different potential risks and rewards. A company in a region with a developing economy, might be able to grow rapidly and see its shares rise quickly in value compared to the UK for instance. However, the fact that the region is still developing means that its economic and political structure could be more subject to change and so this will present more risk to that company’s growth.

Business areas

Different areas of business carry different risk and potential. For instance, oil production seems like a sound business to invest in due to the world’s finite oil reserves however the value of an investment in this business can go down at times of oversupply as seen at the start of 2016. Another example of varying fortunes of a business area would be in the technology sector where a company might bring a ground-breaking development to market only to find that soon after a competitor comes out with an improved version.

The problem with investing directly in bonds, shares or property as an individual is that diversification is expensive because of transaction costs. Other problems include knowing which individual investments to buy and when, and knowing which to sell and when.

Additionally, you may not have the time to keep up-to-date with developments and to carry out the buying and selling of investments at the right moment. Funds offer a solution to these sorts of problems as they invest in a range of investments and are run by professional fund managers.

Funds are offered by asset management companies and let you diversify because the size of each fund means that the impact of transaction costs is relatively low.

Active vs passive

Actively managed funds

The fund manager of an active fund makes investment decisions with the goal of outperforming a particular benchmark, such as an index or the performance of competitor funds.

Actively managed funds may be suitable for investors looking to make potentially higher returns than a fund that simply tracks an index, and/or who want access to more specialised areas (e.g. technology, healthcare or biotechnology).

Due to the time employed in the ongoing task of picking which investments to buy and sell, the fund charges are generally higher than for passive funds.

Passively managed funds

These aim to mirror or track a particular benchmark, such as an index. They still have a fund manager, but the underlying investments are selected automatically in line with the benchmark. For this reason they generally have lower charges than active funds. They’re sometimes called tracker funds as they track an index up and down in value.

Income vs growth

Income

If you want an income from an investment fund you can choose an income share class (sometimes called distribution share class). They use any investment income generated by the fund’s assets to produce periodic cash payments. You can keep this income or reinvest it back into the fund. Look for the ’I‘ or ’Inc‘ next to the fund name to find this type of share class.

Growth

Alternatively if you want growth from an investment fund you can choose a growth share class (sometimes called accumulation share class). This type of share class adds any investment income generated by the assets in the fund back into the fund to increase the share or unit price. Look for the ’G‘ or ’Acc‘ next to the fund name to find this type of share class.

Structured investments

These are products created by investment managers and can be invested in shares, bonds or other assets. They’re designed for investing over a fixed period of time. The terms of the product are set out at the start: the desired return within a range and a specified time frame. They’re sold over a defined period of weeks. After that they start and run for the period of years stated until their maturity date.

Fund of funds

This is where the fund manager invests in a selection of funds. This provides even greater diversification because the fund will typically be indirectly investing in 30-200 shares, bonds or properties for each of the funds into which it has invested. Additionally, a fund of funds can invest in a mix of active and passive funds as well as in specialist funds for specific sectors.

Funds set out their objectives and these can vary considerably.

It’s possible to be very hands-on and choose your own individual investments. For example, choosing specific bonds or company shares and deciding when to buy and sell them. But for most people, especially if you’re new to investing, putting your money into a fund is likely to be a more practical option.

In a fund, your money is added together with that of others and – in exchange for a fee – an expert (the fund manager) makes the decisions. Different funds follow different approaches to help you make the most of your money.

Investing through one or more funds can be particularly helpful if you’ve built up a decent savings pot, want to see if you can get better returns for it by investing, but are not sure where to start.

Would you have the time, skills and resources to choose and manage your own individual investments as well as an expert could?

You’ll naturally take a keen interest in the performance of your investments. But it’s just as important to understand the fees you will be paying, as they can eat into the amount of money you get back from your investments.

Broadly speaking, there are three types of fees: fund fees, platform fees and fees for a financial adviser. It’s important to keep this in mind when planning to invest.

- A platform fee is the charge you pay for the services that an investment platform offers you to be able to continually manage your investment portfolio when and how its suites you.

- Advice fees are the charge for the service and advice you receive from a qualified adviser or online advice tool, they will always be explained before the advice is given.

- Fund fees are the charges you will pay for the fund manager to run the fund. This charge is called the Ongoing Charge Figures and vary by fund, the figure can be found in funds Key Investor Information Documents (KIID). They are always shown as an annual percentage figure, so that you can compare the charge to different funds.

You may need to think about tax when investing. But you could benefit from tax savings, mainly through pensions (either personal or workplace) and Individual Savings Accounts. Your tax treatment is personal to you. It can be a good idea to look at the information available on the gov.uk website and speak to a professional adviser if you’re unsure.

Income tax

When you invest you may also earn income from your investments. And if you do, you might have to pay income tax on that too.

The types of income you can earn from investments include dividends from shares, interest payments from bonds and distributions from funds. Distributions are where a fund passes on your share of any income it earns.

If you’re able to invest in an Individual Savings Account, or ISA, you won’t pay tax on any investment income or investment gains you make in that ISA. To see this year's annual ISA allowance visit our Guide to ISAs page.

For the 2026/27 tax year, you can save up to the annual ISA allowance (£20,000) in cash ISAs, stocks and shares ISAs, innovative finance ISAs and a lifetime ISA. Your ISA limit can be paid into multiple ISAs of the same type, except the lifetime ISA, each tax year.

The dividend allowance lets you receive up to a set level of dividends, free of income tax, in each tax year. And, depending on your circumstances, the personal savings allowance potentially lets you receive up to a set level of interest from investments and savings, free of income tax, in each tax year.

Capital Gains Tax

This is the tax you’ll have to pay on the profit you make when you sell your investment. You only have to pay this tax if the amount you receive from selling your investment is above your annual tax-free allowance for capital gains.

Inheritance Tax

Your family may have to pay this after you die if you leave assets worth more than a certain amount, including investments, and depending on who you leave them to.

You can find out more about taxes on the gov.uk website which includes all the latest tax rates and tax allowances that might be relevant for your personal circumstances.

Perhaps the most important thing to remember about investing is that you never have to go it alone. A broad range of information sources and support is available, whether you’re just starting out, or looking to build your knowledge. In some cases, you can use the information to make your own decisions, while others will give you advice and then put it into action on your behalf.

You might want to speak to friends or family who are a little more experienced.

Or if you want help to decide, for example how much risk to take or what type of investment might be best for you, then one of the online digital advisers may be able to help. You can also speak to a financial adviser about your investment goals and how you might seek to achieve them. Whether going online or speaking to an adviser, you will pay a fee for professional financial advice.